FOR YOU

Collegia is your personal, Auto Enrolment, workplace and self-employed pension, all in one single account and intuitive app.

Get started

Your pension professionally

managed

Your money is invested by one of the

world’s premier asset managers

Invest with the help of

the government

A 25% top-up is collected automatically,

every time you contribute

FCA regulated and

FSCS protected

Your pension is insured once

it’s invested with Collegia

Managing how you plan for your retirement is much simpler if all your pension savings are in one place. The Collegia Pension allows Auto Enrolment contributions from multiple employers at the same time, plus it’s a personal pension, so you can add income from any self-employment or just top up as you please.

No form filling. Your Collegia Pension makes managing your money easy. We automatically collect the 25% boost from the government on your behalf and you can see it in your account as it arrives.

Our proprietary technology gives members complete control over their pension. With real-time access from any device, they can track contributions, project retirement savings, and adjust investments on the go. And because pensions should be easy for everyone to understand, Collegia speaks your language — literally.

Our platform supports over 100 languages, making it simple for members to manage their pension in the language they’re most comfortable with. We use secure, intuitive digital tools to help every member make informed decisions and feel confident about their financial future.

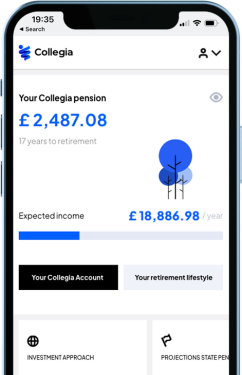

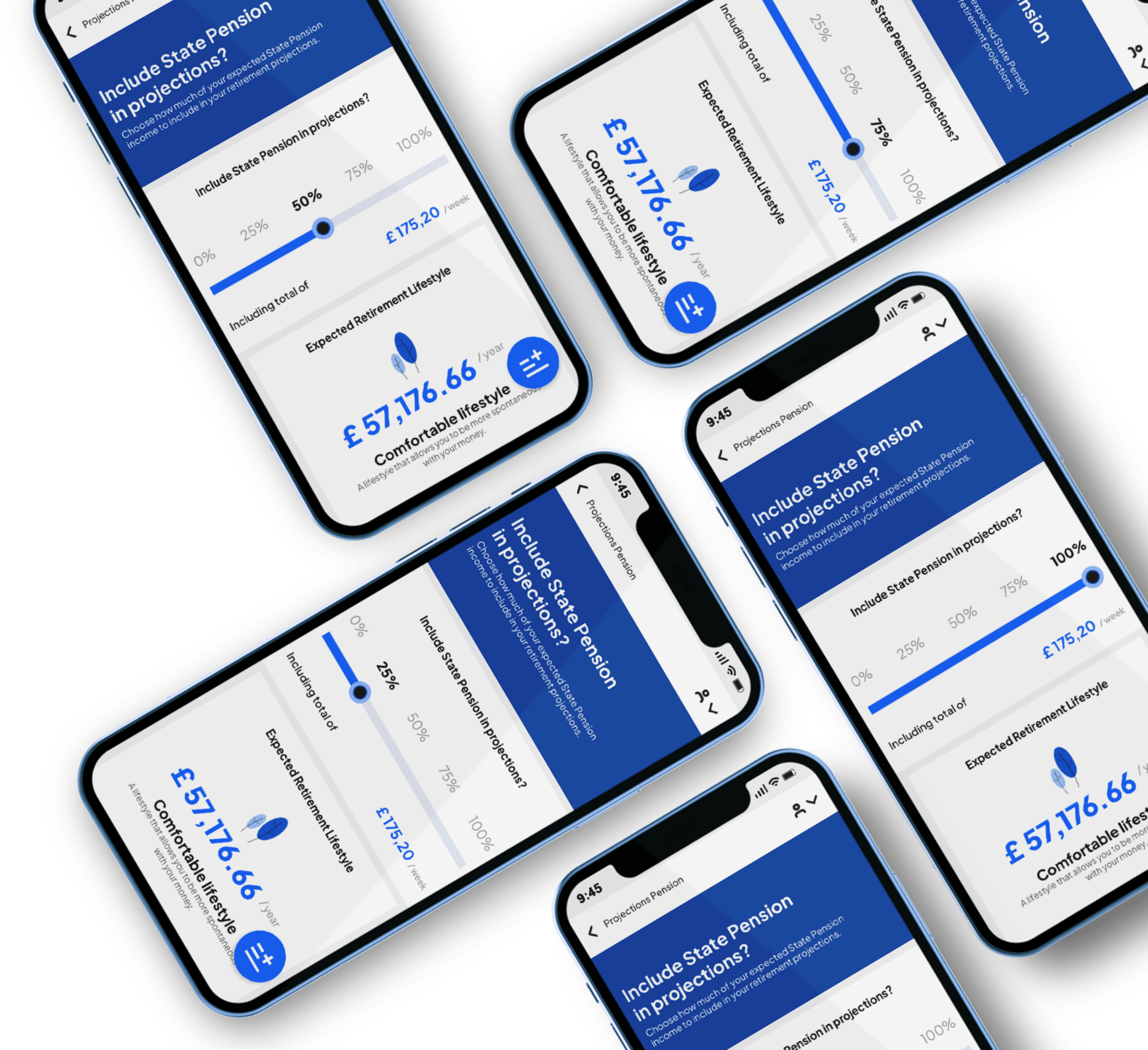

Your retirement isn’t just about a savings balance — it’s about the life you’ll be able to live

Our personal application shows you, in real time, the lifestyle your current savings and contributions are likely to support in retirement. Instead of abstract projections, you’ll see practical insights based on everyday spending categories such as housing, groceries, travel, and leisure.

As your situation changes, your projected retirement lifestyle updates instantly — giving you a clearer picture of what the future could look like and what steps you can take to improve it.

Download the Collegia Pension App

Start saving now if you are self-employed or looking to top up your pension

Talk to your employer about paying your Auto Enrolment pension directly into your Collegia Pension

We will add your 25% government top up automatically

Register all your current pension pots on the App to see your total retirement picture and don’t worry, unlike other providers we don’t ask you to transfer them – unless you feel it’s the right thing to do.

Here are some explanations about how Collegia works.